Summary: If you need business funds without putting your home or equipment on the line, this guide shows what unsecured business loans need from you and how fast the money can land. You skip the asset valuation and get faster…

Summary: This guide breaks down how car finance works in plain language, so you can walk into any dealership knowing what a fair deal looks like. Most car loans are secured, where the car is the security, so the rate…

Summary If bad credit has you worried about car finance, here is what actually matters, how these loans work, and what makes getting approved as quick and easy as possible. Bad credit alone does not automatically rule you out. Specialist…

Summary You've found the car. Now comes the part most buyers rush: the finance. A dealer offer on the desk feels fast and easy, and at first glance it often sounds like a great deal. That is exactly why it…

Summary You have probably seen the ads for an EV novated lease. They are everywhere right now. The noise comes from the current Fringe Benefits Tax (FBT) exemption, and the government's decision to wind it back in March 2027. The…

Summary: Payday super begins July 1, 2026. If you employ staff, your cash flow obligations change from the first pay cycle. This post covers what that means for your working capital, what finance options can bridge the gap, and why…

Summary: With 4x4 holidays becoming more popular and the choice of many Aussies, Finance for 4WD has become a huge market. What has become equally as common is people who have just financed a new 4x4 looking for an additional…

Summary: Simplify your wedding planning with expert guidance, helping you budget, compare options, and secure the right finance without stress. Plan your borrowing by calculating exact needs, understanding rates and fees, and choosing a repayment term that fits your budget.…

Summary: Choosing between new and used business equipment comes down to balancing cost, technology, and risk; equipment finance can make either option accessible. New Equipment: Offers the latest technology, warranty protection, and lower early maintenance but comes at a higher…

Summary: Make your dream wedding achievable by combining costs, getting repayments that fit your budget, and protecting your savings. Choose between secured or unsecured loans and fixed or variable interest rates to suit your needs. Avoid high-interest credit cards and…

Summary: The EV market has changed fast. More models, more price points, and more reasons to look seriously at making the switch. Here's what you need to know before you decide. The EV market now covers a wide range of…

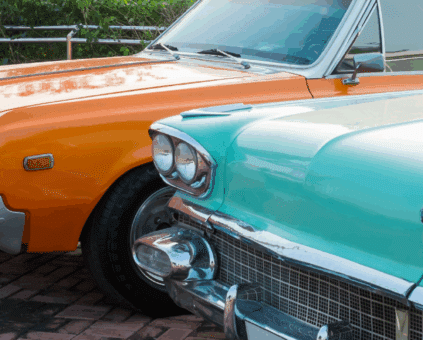

Summary: Caring for a vintage car doesn’t have to be complicated. Focus on key areas and always consult a qualified mechanic to enjoy your classic without stress: Regular mechanical maintenance, fluid checks, and battery care keep your vintage car reliable.…

Summary: This guide explains how businesses can secure the right equipment finance to grow, outlining practical funding options and how to improve approval outcomes. Equipment can often be used as security, with specialist lenders offering flexible solutions beyond the big…

Summary: Low doc car loans make it easier and faster for self‑employed workers and business owners to get the vehicle they need without being held back by heavy paperwork and traditional lending requirements. Less paperwork, faster approvals: Simple documents like…

Summary: Get the right truck finance for your business with flexible terms, competitive rates, and expert guidance to keep your cash flow healthy and decisions stress-free. Compare multiple lenders for new or used trucks with terms that suit your business.…

Summary: Buying a car is exciting, but understanding car loans can be confusing. Fox Finance Group guides you through your options so you can make confident decisions and secure the right loan. Car loans can be secured (lower rates, car…